Home Ready Dti Limits

Home ready dti limits

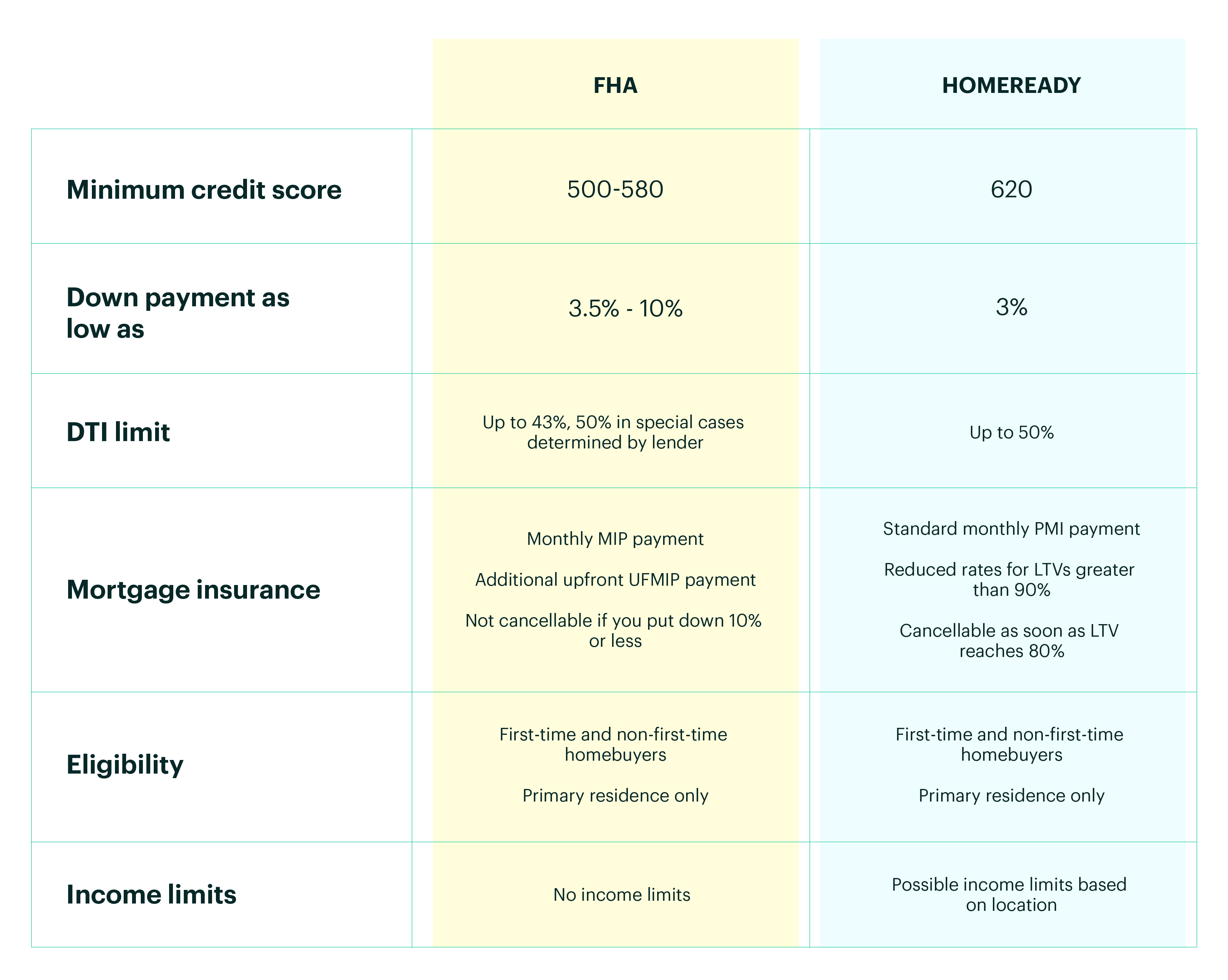

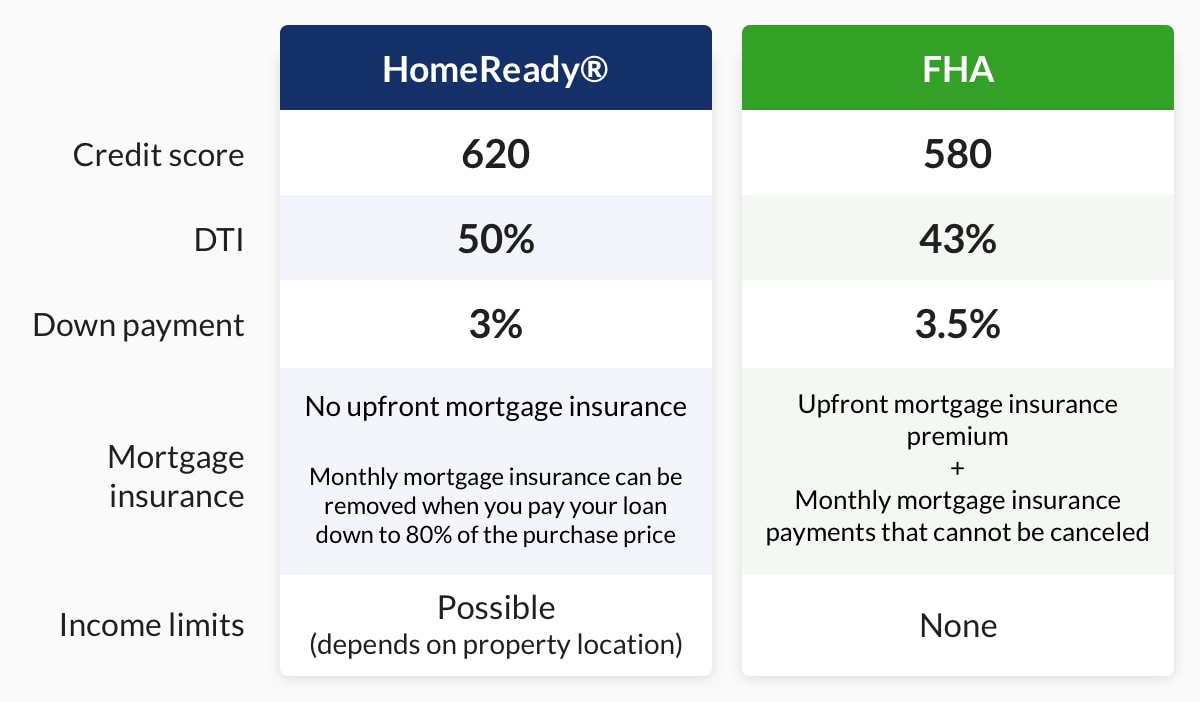

Fha Vs Homeready Better Mortgage

Fannie Mae Homeready Income Limits Mortgage Guidelines

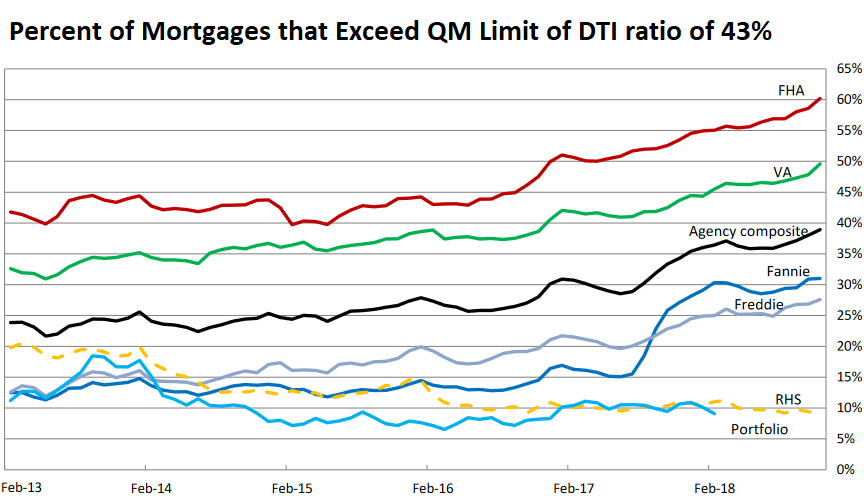

Https Www Fanniemae Com Resources File Research Housingsurvey Pdf Max Dti Ratio Pdf

Https Singlefamily Fanniemae Com Media Document Pdf Homeready Product Matrix

Fannie Mae Home Ready Overview Naihbr

Fha Debt To Income Dti Ratio Requirements 2019 Fha Mortgage

First time or repeat homebuyers.

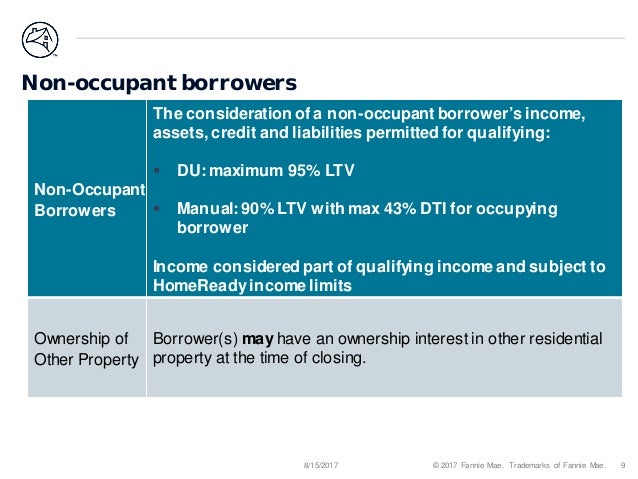

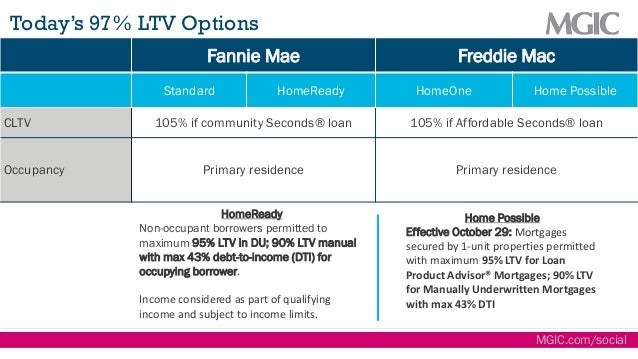

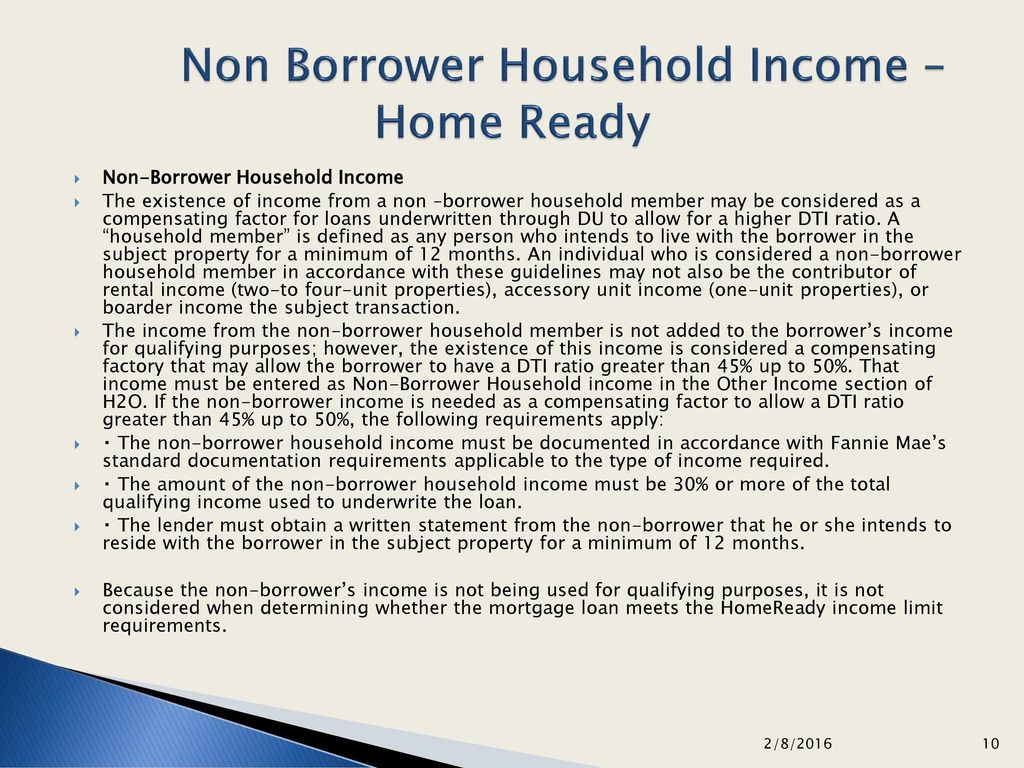

Home ready dti limits. There is no income limit on properties in low income. Credit score 620. The maximum can be exceeded up to 45 if the borrower meets the credit score and reserve requirements reflected in the eligibility matrix. Non occupant borrowers non occupant borrowers permitted to maximum 95 ltv in du.

This limit is revised annually. 90 ltv manual with max 43 debt to income dti for occupying borrower. For loan casefiles underwritten through du the maximum allowable dti ratio is 50. Borrowers with credit scores 680 may get even better pricing.

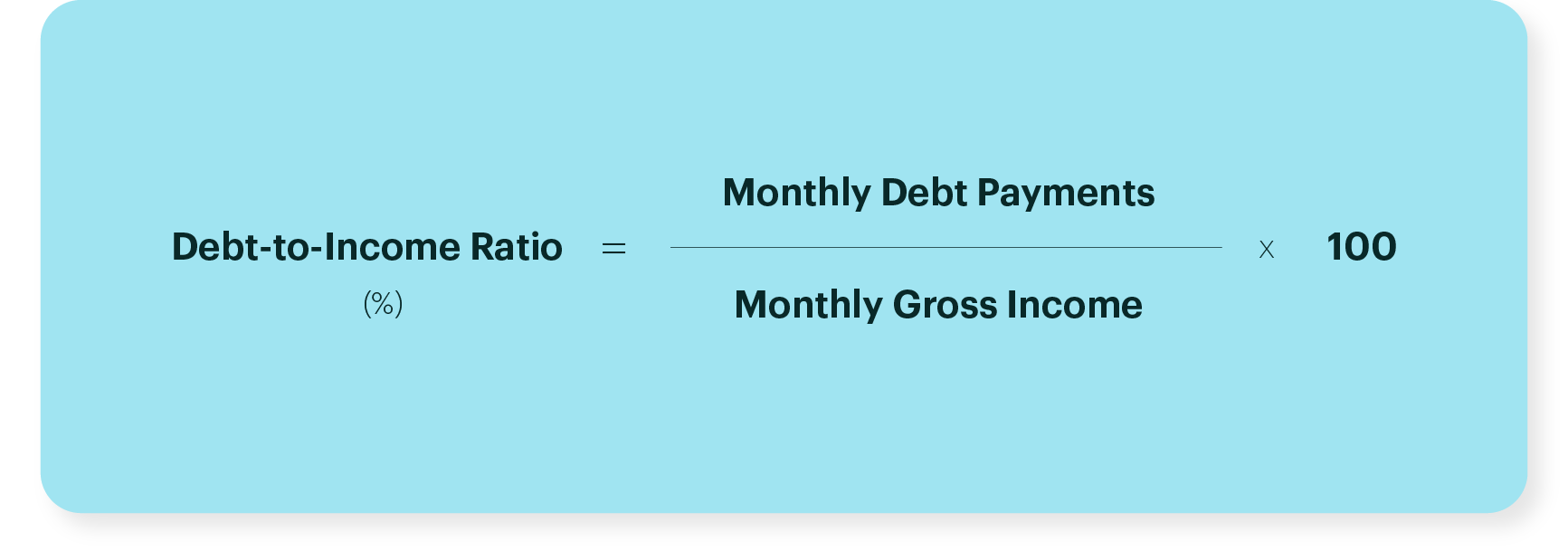

Looking to purchase a home for their multi generational family. For instance someone making 4 000 per month and 2 000 in housing credit card and student loan debt payments would have a 50 debt to income ratio. Limited cash for down payment. Income considered as part of qualifying income and subject to income limits.

The maximum debt to income for homeready is 45. With an fha loan the dti limit is 43. Borrower income must be below 100 percent of the area median income ami with some exceptions based on the property s location. Supplemental boarder or rental income.

With a homeready loan the dti limit is up to 50. Credit scores as low as 620 are permitted. Normally such a home buyer would not qualify. Have a credit score 620 have a higher debt to income dti ratio no more than 50 have or are interested in having supplemental rental income fha va conventional and usda loan requirements are subject to change.

Homeready allows for nontraditional credit. This option offers extreme flexibility and make it easier for low income families purchase a home. Have limited cash for a down payment.

Kentucky Fha Loans Compared To Kentucky Conventional Loans First

Https Singlefamily Fanniemae Com Media Document Pdf Non Occupant Borrower Income Flexibility

How To Calculate Debt To Income Ratio For Home Loan Google

Todays 3 Percent Down Mortgage Options 2019

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcra7gtyjubznxbvsq2v1ko Tdm Xb3glhtcnw Usqp Cau

Kentucky Fannie Mae Loans Versus Kentucky Fha Loans Fha Loans

How To Lower Your Debt To Income Ratio Dti For A Mortgage

Homeready And Homepossible Presented By National Mi And Fairway

Debt To Income Dti Ratio Guidelines For Va Loans

Louisville Kentucky Mortgage Lender For Fha Va Khc Usda And

Dti Ratio First Time Homebuyer Dream Thief

First Time Home Buyer Qualifications What You Need To Get Approved

Pin On First Time Homebuyer Info

Http Nymc Org File Download Inline 4763c3cd 1cd1 439e 8581 A75c40bb79e6

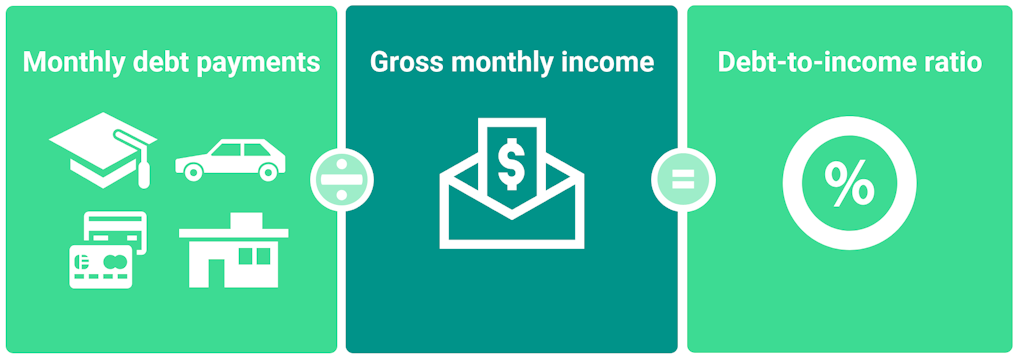

Defining Your Dti Ratio

Eqdtmadhpbzd7m

Ca Down Payment Assistance Programs 580 Fico County City

10 Biggest Benefits Of Va Home Loans In 2020

Essex Offers Home Ready Du Home Possible Lp 2 8 Ppt Download

Fannie Mae Home Ready Program For Kentucky First Time Home Buyer

Fha Home Loan Requirements Blog Missouri Usa Mortgage

Homeready And Home Possible Loans With 3 Down For 2018 Kvue Com

Debt To Income Ratio Requirements And Factors That Influence It

Va Loan Max Dti For Va Loan

What Is Debt To Income Ratio And Why Does It Matter Credit Karma

How To Get Pre Approved For A Mortgage

Knowing Your Dti Ratio Keybank

Https New Content Mortgageinsurance Genworth Com Documents Training Course Agency 20updates 203rd 20qrt 202017 20finalmk Pdf

Shadow Banks Dominate Mortgage Lending By Piling On Risks

Jumbo Loans What They Are Limits Rates More Rocket Mortgage

Https Www Nchfa Com Sites Default Files Forms Resources Homeadprogramguide Pdf

Https Www Mgic Com Media Mi Underwriting 71 40600 Guide Pdf Underwriting Guide Pdf

Https Www Vhda Com Businesspartners Lenders Loaninfoguides Loan 20information 20and 20guidelines Fnma Reduced Mi Program Guidelines Pdf

Single Family Home Is It The Best Option For You Mortgage

Freddie Mac Enhanced Relief Refinance Guidelines For 2019

Upfront Guarantee Fee Will Change From 2 75 To 1 0 Annual Fee

Https New Content Mortgageinsurance Genworth Com Documents Training Course Lpa Advancedguidelines Presentation 1119 Pdf

Home Loan Programs Assistance Get Home Financing At Apm

How Much Can I Borrow With A Va Loan

Guardian Mortgage Home Buyer Guide 2019

3 Ways To Manage Your Debt And Still Buy A Home

What Is A Good Debt To Income Ratio For A Mortgage Intuit Turbo Blog

Mortgage Refinance Requirements Rocket Mortgage

Indiana Housing Community Development Authority Servicer Overlays